This is the 10th article in my series on launching tokens in Canada. This post contains some of the practical tips that I've given to token projects over the last few years (all of which have not had any regulatory or private legal actions against them). The goal is to minimize risks while selling, both in the initial phases of a project and later. The latter part of this post concludes by explaining how securities laws impose a useful type of discipline that moves people away from failed projects and short-term thinking. Following the law can be a powerful advantage in the market.

Conservative Rules Of Thumb For Selling

Before getting into the different ways to sell and the issues, what are the rules of thumb for avoiding securities law problems when selling tokens?

A. Don't talk about future functionality in connection with selling tokens

B. Don't engage in price speculation before or during token sales

C. Don't sell in advance of a token being minted

D. Prefer secondary over primary sales

E. Consider raising capital to get to launch, then selling tokens once the system exists

F. Don't over-promise

G. Describe tokens and systems in technical terms, not business terms

H. Don't publish tokenomics diagrams

The rules of thumb below apply only until all the tokens are sold. Once a project isn't going to be involved in selling tokens anymore, there are fewer or no issues. But even before that, these rules are really guidelines that help to understand the issues, which are explained below.

Free Crypto: Modern Projects Aren't Like Bitcoin

When considering how to minimize the downsides of Canadian laws (and maximize the upsides of being a Canadian project), the best thing a token project can do is to give away the tokens. With Bitcoin, this took place through cryptocurrency mining. That wasn't intended as a legal solution, but it avoided the investment contract

question (see part 3 of this series).

Free vs. Paid

There's a strain of thinking that infects many areas of law: things that are free shouldn't have high burdens on the people who provide them. This similarly applies with securities law, where giving away a token might completely sidestep legal concerns. But this isn't very useful advice for most projects, where there is not a super-programmer like Satoshi Nakamoto willing to produce public goods for nothing. In real life, most of the time, things cost money, and anybody making an interesting system needs to figure out how to pay for expenses (like programmers, servers, managers, lawyers, accountants, etc.).

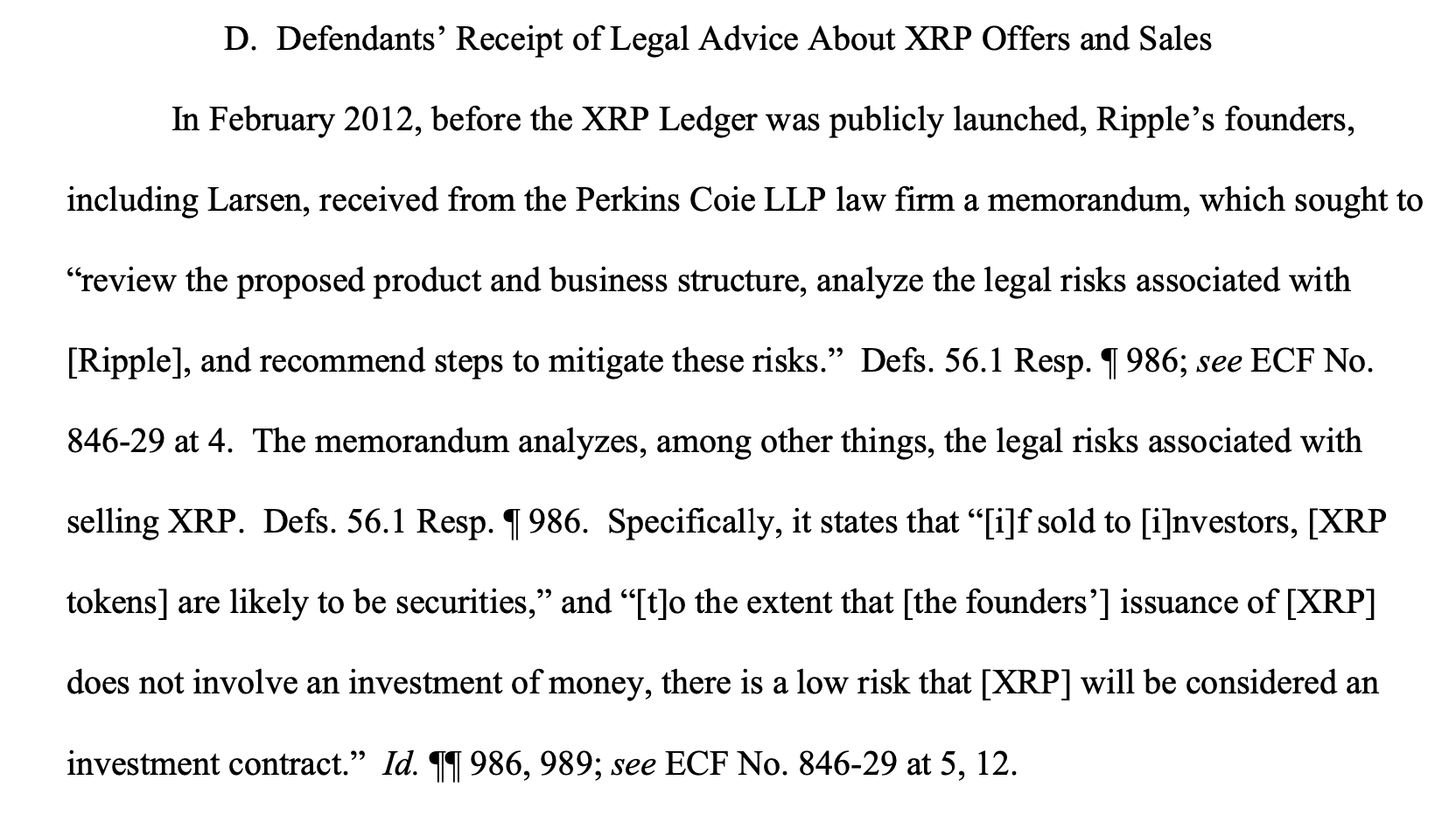

What if it's free? Great lawyer thinking (and even features in the 2012 advice that Perkins Coie gave Ripple in the landmark 2023 decision). Not very useful. But yes, if a token isn't sold and is merely given away, probably there's little to discuss with securities laws.

System Exists: Raising Capital vs. Selling

A system that doesn't exist yet will be far more likely, in connection with a token, to be seen as a capital raise (see part 5). This is how investment works: people give money to build a business and launch a product or service. The investment is necessary because the thing does not yet exist to be sold. But if the thing does exist, and is being sold, it's far more likely to be seen as a commercial sale.

Where there is an already operating system that generates some sort of return for the token holders, it's also important to ask whether that's due to the activities of management or not (part 8).

So the first question is: does the whole system exist, with all of the elements? If the answer is that some of the elements haven't been made yet, the project needs to consider scaling back their marketing and only talking about what actually exists. Many people have gotten into legal trouble by saying what their vision is, selling tokens, and then building that vision. If instead they merely described what exists right now, and sold tokens for it, they'd have a lot fewer problems.

Token(s) Exist: Presales vs. Post-Launch Sales

The more uncertain the nature of the thing being bought, the more likely it will be viewed as an investment and not as a commercial sale. Presales are normal, and routine in many industries, but many crypto projects have run into trouble by conducting presales that look a lot like an early investment round.

The worst type of presale of a token is where the token does not yet exist at the time of the presale. This can almost always be avoided by simply making the token on-chain! If the token exists, it's merely a matter of waiting until it's delivered. If the token doesn't exist, it's a more speculative question about what the buyer will receive. There's a lot more room to argue that the nature of what is being sold was not as definite, and therefore more likely to be in the nature of investment. Investment is generally into a broad idea of a business, whereas sales are generally of a specific thing.

Presales should be for a specific thing, and the more specific the better. But they should not be for future things that don't yet exist. Too many projects want to talk about roadmap, and the amazing things that will one day exist, but there is both a securities law problem with that and also a practical problem: what if it doesn't happen? Marketing people and visionary CEOs love to think that their optimistic visions will come true, but the reality of software is that there are delays, unexpected challenges, and pivots. Functionality that might not exist ought not to be promised.

Presales that are too far in advance of delivery are vulnerability. Presales that are too vague are vulnerable. Presales that are too specific, about things that don't exist/might never exist, might even be fraudulent.

Market(s) Exist: Primary vs. Secondary

If a token is sold directly by a project to a buyer there's a much higher chance of that being investment then sales into an established market. This is at the heart of the 2023 Ripple decision (settled in 2025 for $125m).

When a person buys a token on a marketplace they don't know they're buying from the creator of the token, and so it's much harder to have a subjective intent of contributing capital to something. In the case of Ripple, 99% of market volume was not Ripple itself transacting, and the judge found this to be a very persuasive fact in determining that people couldn't have had a subjective intent to invest when almost certainly their buy transaction wouldn't result in money in Ripple's pockets.

Primary sales are when projects sell to a specific buyer, with a contractual relationship between them. Primary sales are much more likely to attract regulator scrutiny.

If a project sells its own token on a secondary market, and there's a lot of other trading activity, that's a great fact. If there's no other trading activity because, for example, it's a DEX launch and all the liquidity is from the project, then this is less favourable. But at least with a DEX launch it's harder to make representations to buyers.

The type of market sale is really about the representations made. Large token buyers (common for primary sales) usually ask due diligence questions, and if those are answered, those are probably representations. It's very difficult to sell a lot of tokens to a sophisticated buyer without making representations, and these should always be carefully scrutinized. This is important for seecurities laws, but also because the buyers might sue on the misrepresentations that might be made by eager salespeople. When people are in selling mode they do not tend to speak like lawyers.

Representations Define The Sale

Over and over again, the case law and regulatory actions show people who wanted to convince people to buy, and said something they shouldn't have. If they had only stuck to an accurate technical description of what they were doing, their problems would have been avoided. When I work with teams I constantly hear that they have to

say these things to get a sale. Well? Then you're taking a risk. Businesses are all about risk, so that may be fine, but it's rare people truly understand the risk they're taking. They know they're about to get millions now, and maybe problems later - is that a hard decision? It takes significant restraint (which comes from leadership) to make sure a token has a durable future, free of securities law problems and lawsuits from disappointed purchasers.

Projects should talk about the technical merits of what they're building. Most of the time, with crypto, there's technical details. If there's purely business details; describe them fairly, honestly and accurately. When tokens & systems are accurately described they're far less likely to be illegal securities.

Tokenomics Diagrams: Don't Do It

I always advocate against publishing tokenomics

diagrams. Everyone involved in crypto has seen these. They're a pie chart showing who gets what, and how money will be spent. Often they contain detailed budgets, and explain how much marketing will be done with $X. They are created largely because other people create them (and thus become a sort of informal standard), and to a lesser extent because some buyers/exchanges demand to see them.

Tokenomics is sort of astrology for crypto, or perhaps more generously: technical analysis. Buyers want to know a bunch of numbers and plans, so that they can guess at how the token will perform, with the assumption that the numbers help with the analysis. I'm skeptical that they empirically do help with knowing the future, and if this is true, then perhaps it's fine to publish these because they have no meaning at all! But probably they're still relevant to the legal analysis even if they're useless, because they're representations that may be used as part of a decision to buy.

It would probably be better if everyone stopped publishing tokenomics diagrams, but in the world where they're required

, projects should know they're taking added risk by publishing these kinds of documents. The risks involved and details are a bit too complicated to toss into this already quite long blog post series, but suffice to say that nobody is doing themselves a legal favour by publishing a tokenomics diagram.

Short-Term Thinking With Selling

A great many problems in crypto are due to short-term thinking. A project that sells a token now, that's deemed to be a security later, may cause their tokens to be delisted from exchanges/dealers - a very bad outcome. That said, since most tokens are not in and of themselves securities (part 9), this is more likely to just create regulatory liability or potential litigation from disappointed buyers, rather than fatally condemning the token to being a security.

Many people have correctly concluded that because the chance of regulatory action or lawsuits from buyers is very low, they should discount this risk and do whatever improves sales. Some lawyers oblige these kinds of founders, but they're doing a disservice to their clients and the law by doing so. Usually with only a few changes, a project can have a drastically lower risk of problems.

Canadian Regulatory Action

Canadian projects that sell tokens are at higher risk of enforcement action by their local regulators than foreign companies. I wish this wasn't the case. I wish regulators enforced the law equally against projects that sell to Canadians, no matter where they are based, which would align with the law. That is not the case, and it's a widely known fact that regulators aggressively target local companies and essentially ignore the much larger world of bad actors abroad. This is unfortunate, but it just means that Canadians need to do an extra-good job, which isn't such a bad thing.

There are advantages to operating lawfully in Canada. A Canadian business that develops a successful model can more easily attract investment than a Cayman/BVI/Seychelles/Panama/Cyprus/etc. offshore entity. The trade-off of going offshore is complexity, cost, and lower investability. A Canadian company may have to sell more conservatively, and may have to choose methods that are lower risk, but the upside is probably a more sustainable business, and certainly a more investable one. Projects that are merely about a money grab right now have soured everyone on the space, and continue to take away attention from the people building interesting and good businesses based around tokens.

Yes, it's hard to come up with useful, good, lawful ideas for tokens. Most people won't come up with the next DEX idea, decentralized lending concept, or algorithmic stablecoin. Innovation is hard. Tokens are still not that widely used in the general economy. The problems are well known. But the projects that crack these problems stand to make fortunes for themselves, and immensely benefit the world because crypto systems are global by default and can serve gigantic user bases at extremely low costs. We are still in the early stages of discovering what this new technology can do, and anyone who looks only to the bad investment schemes, frauds, and failed dreams is ignoring the impressive technological development that's happened over the last 15 years.

Following the tips in this blog post will probably make selling tokens more difficult, and might reduce the initial amounts made from selling, but a long-term business can likely sell more tokens later when it's fully established and popular. Many crypto projects are focused entirely on tomorrow and not on what would happen if they succeed. Selling too many tokens early in the process might be disastrous when compared to how much more money could be made by selling later. The price graph for almost every successful crypto project shows a huge run up over time, which supports the idea of holding tokens as a war chest for later. Best of all: the tokens sold later are far less likely to attract securities problems.

Long-Term Thinking

Interesting things cost money, and investors aren't the only way to get that money. It's possible for a project to sell a token and use that for building interesting things, but it has to be done in the same manner as Nike selling shoes so that they can do more R&D on shoes.

The more a token looks like selling shoes, the less likely it will be to have problems. This sometimes requires a degree of long-term thinking, but I continue to believe that the best blockchain projects are the ones that think long-term, don't sell too much too early, and are honest and accurate about what they're doing. Following Canadian securities laws doesn't have to be a negative. Following the law can actually be positive for a project because it requires making changes that are ultimately usually quite healthy for long-term success.